The construction industry is a massive part of the economy. In 2025, it employed 8.3 million people and generated $2.2 trillion in annual spending.

Because of this high demand, many skilled tradespeople eventually decide to go into business for themselves. But working on a job site and running a company requires completely different skills. When you own the business, your focus shifts away from the physical work. You have to manage cash flow, secure city permits, and price out jobs so you actually make a profit.

If you are ready to make the jump from employee to owner, you need a straightforward plan. This guide walks you through the eight steps to start your construction business, organize your operations, and learn how to bid on construction projects in your local market.

Key Takeaways

- Running the business is a completely different job: Being a great tradesperson does not automatically make you a great business owner. You have to shift your focus away from the physical labor and prioritize managing cash flow, legal compliance, and accurate pricing.

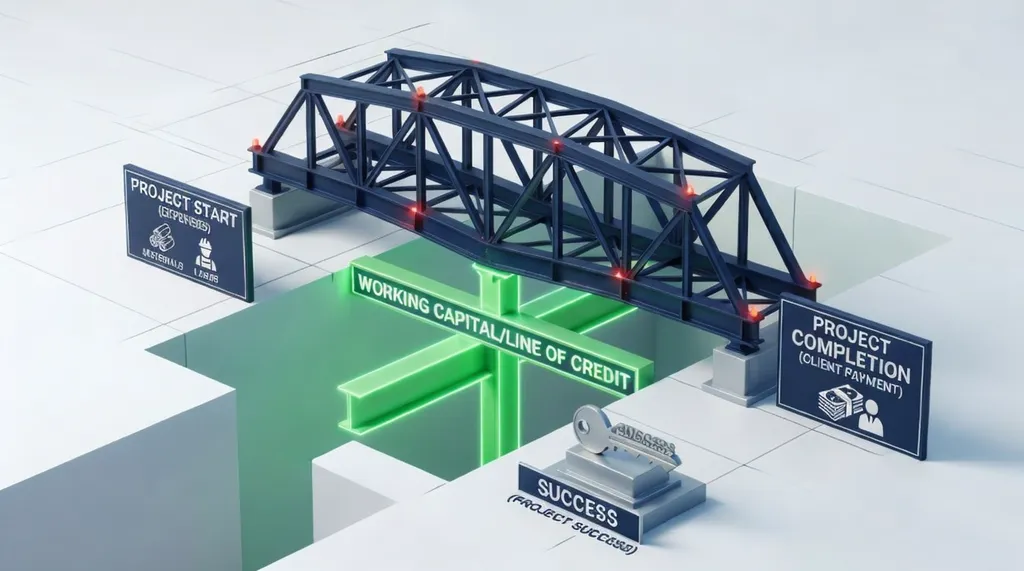

- Cash flow will make or break you: Construction operates on long payment cycles. You need enough working capital or a dedicated line of credit to pay your crew and buy materials weeks before the client’s invoice actually clears.

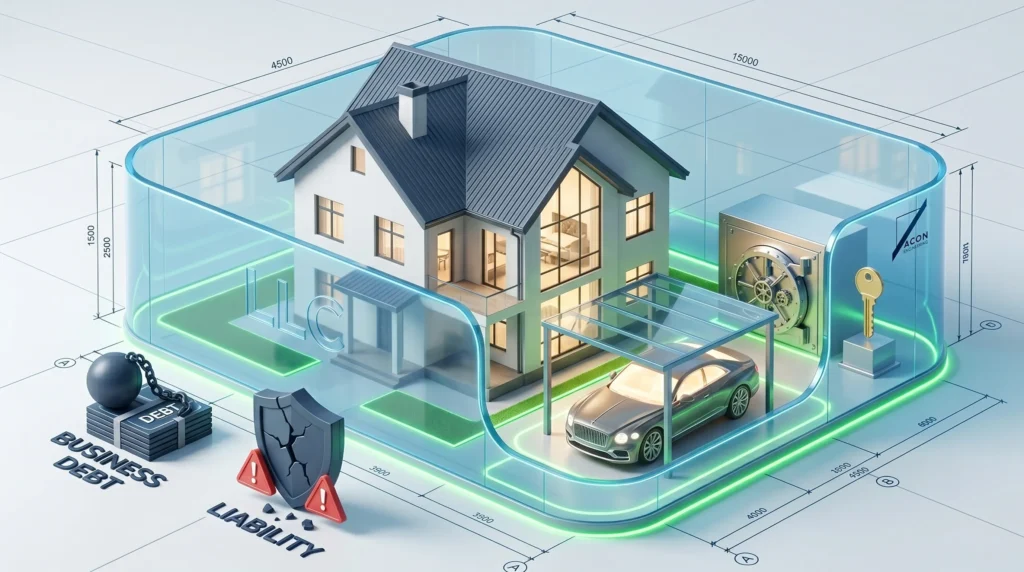

- Protect your personal assets early: Setting up an LLC is usually the smartest move for new contractors. It creates a necessary legal wall between your business debts and your personal bank account.

- Accurate estimating protects your profit: Guessing on material costs or labor hours is the fastest way to lose money on a build. Outsourcing your estimates to professionals gives you precise numbers and frees up your time to actually run the company.

- Relationships drive your early growth: Treat your subcontractors, local material suppliers, and city inspectors well. Your first few projects will almost always come from your existing network and word-of-mouth, not from expensive internet ads.

What is a construction business?

A construction business is a company that plans, builds, remodels, or maintains physical structures. These companies typically operate as either general contractors who oversee an entire project or specialty subcontractors who handle specific trades like plumbing, electrical work, or roofing.

The primary goal of a construction company is to complete building projects safely, on time, and within a set budget. The services provided depend entirely on the company’s chosen niche. This can range from residential home framing and commercial office fit-outs to large-scale industrial site development. The unique value of a construction business is its ability to organize raw materials, specialized labor, and heavy equipment to create functional spaces for clients.

How is it different from other businesses?

Running a construction company is entirely different from operating a retail store, a restaurant, or a digital agency. The business model is project-based. You do not rely on a steady stream of daily sales. Instead, you secure large contracts that dictate your workflow and cash flow for months at a time.

Here are the main factors that make construction unique:

- Longer payment cycles: You rarely collect full payment upfront. Construction uses a milestone payment system. This means you often have to pay for labor and building materials out of your own pocket long before the client pays your invoice.

- On-site variables: Most businesses control their working environment. A construction site is exposed to unpredictable weather, delayed material shipments, and sudden structural changes that force you to adjust your plans on the spot.

- Strict regulations and safety: Construction carries high physical liability. You have to follow strict safety codes, secure local building permits, and pass ongoing city inspections just to keep your job site open and legal.

- Complex project management: You are not just managing your own employees. You have to coordinate multiple independent subcontractors, schedule material drop-offs, and constantly adjust your timeline to keep the project moving forward without costly delays.

How to Start a Construction Company (A 9-Step Process)

Starting a construction company requires moving systematically from market research to legal registration, securing funding, and setting up your operational workflow. If you try to skip steps, you risk severe legal penalties or running out of cash before you finish your first project.

Step 1: Research your local market and competition

You have to know exactly who you are selling to and who you are up against. Start by analyzing your local demographics to understand actual market demand. You need to know if your area is filled with young families buying older homes that need remodeling, or if developers are funding new commercial spaces. Contractors targeting the home improvement market often rely on professional Remodeling Estimating Services to prepare accurate budgets and competitive bids for renovation projects. This information helps you lock in a specific niche instead of trying to offer every service possible.

Once you know your focus, check the current local rates so you understand what the market can actually support. You then need to research your direct competitors to figure out their service offerings and pricing structures. Read through their customer feedback closely to look for recurring problems.

If you see a consistent pattern of clients complaining about poor communication or messy job sites, you have just found a gap in the local market. You can use those exact weaknesses to build your Unique Selling Proposition, giving clients a clear, direct reason to hire you instead of the established competition down the street.

Step 2: Write a Comprehensive Business Plan

Your business plan is the formal document that proves to banks and investors that you know how to run a profitable company. Instead of a massive wall of text, break your plan down into these specific sections:

- Executive Summary: A clear, one-page overview of your company’s mission, your physical location, and your Unique Selling Proposition (USP).

- Company Overview: A direct list of the exact services you provide and the specific construction niche you are targeting.

- Market Analysis: Proof that you understand your local area. You should include your target buyer personas, current building trends, and a realistic SWOT analysis (strengths, weaknesses, opportunities, and threats).

- Management and Team Structure: Investors invest in people. Detail the “faculty” of your business, who are the founders, project managers, and outside advisors (like your CPA or lawyer) running the day-to-day operations.

- Sales and Marketing Strategy: A practical breakdown of exactly how you plan to position your brand and acquire your first local clients.

- Financial Plan: The most important section for lenders. This must include your projected cash flow, monthly overhead costs, and your expected profit margins for the first three years.

Step 3: Choose your legal business structure

Your legal structure dictates how you file your taxes and how much personal risk you take on if an accident happens on the job site. Here are the main options you need to consider:

- Sole Proprietorship: This is the easiest and cheapest way to start if you are working completely alone. However, it is highly risky. If a client sues the business, your personal assets, such as your house and personal bank accounts.

- Partnership: If you are going into business with someone else, this structure allows you to split the startup costs and the daily workload. Just remember that both partners share the financial and legal liability.

- Limited Liability Company (LLC): This is the most common choice for new contractors. An LLC creates a legal wall between your business debts and your personal savings. If the company goes bankrupt, your personal assets remain safe.

- Corporation (C-Corp or S-Corp): If you are building a massive operation and need serious funding from outside investors, a corporation offers the highest level of legal protection. The downside is that corporations require strict record-keeping and deal with much more complex tax computations, including potential double taxation.

Step 4: Register your business and obtain licenses and permits

Construction is a highly regulated industry, and operating without the right paperwork can shut your business down fast. Start by registering your business name with your Secretary of State and getting an Employer Identification Number from the IRS so you can open a bank account and hire employees.

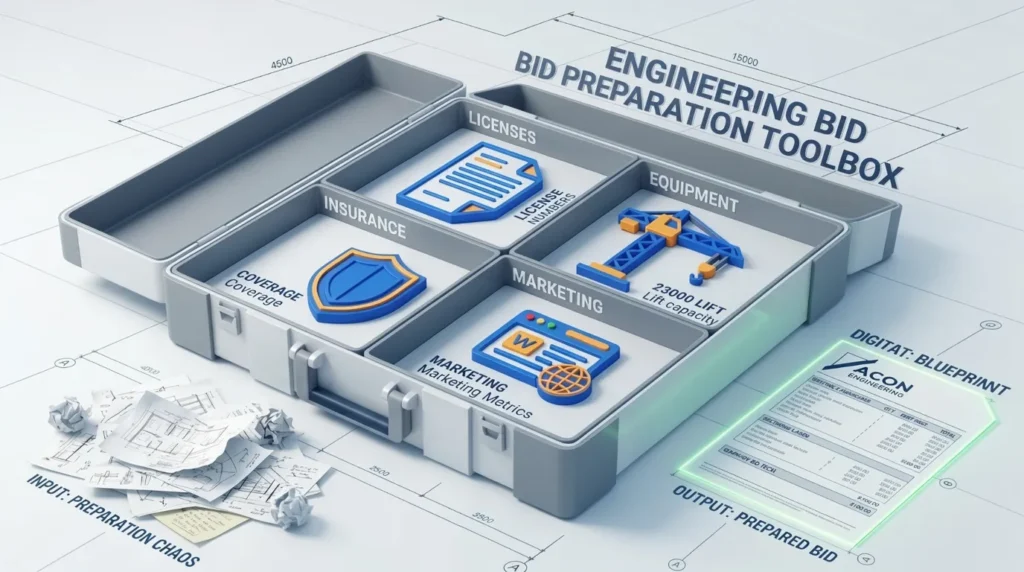

Next, you have to handle state licenses. For example, if you work in California, you must register with the Contractors’ State License Board and pass specific trade and business exams. If you do specialized work like plumbing, electrical, or HVAC, you will need separate occupational certifications. On top of state rules, every local city has its own requirements for general business operating licenses and specific building permits for every job site.

You also have to buy insurance, which includes general liability, workers’ compensation, and surety bonds. If you have a physical office or equipment yard, you will need property insurance, too. Before you file all this paperwork, it is a great idea to talk to established contractors in your area. They can tell you exactly which local permitting offices are the slowest and what specific problems to watch out for.

Step 5: Secure funding and set up construction accounting

Construction uses up cash very quickly. Standard accounting methods usually fail in this industry because you do not have steady daily sales coming in. Instead, you need a financial system built specifically to handle project phases and long payment cycles. First, calculate exactly how much money you need to survive each month to cover truck payments, insurance premiums, and basic payroll, even if no client checks arrive.

To fund this, you can apply for SBA loans or traditional bank loans for lower interest rates. Private lenders are an option if you need cash fast, and you should also look for specific grants if you focus on energy-efficient building. Lenders will want to see clean financial statements that prove you understand your overhead and profit margins.

You absolutely must set up job costing, which means tracking exactly how much labor and material go into every single phase of a project. If you just look at your main bank balance, you will never know which jobs are actually making a profit. Getting a dedicated construction line of credit will also help you pay for lumber and labor while you wait for clients to pay their milestone invoices.

Step 6: Invest in a lean team and build a professional network

Construction is a relationship-based business, and your company is only as reliable as the people working on your job sites. Before you take on the financial stress of full-time payroll, it is usually better to hire trusted specialty subcontractors. Make sure you vet them for quality work, punctuality, and proper insurance coverage. You also need to open accounts with local material yards and hardware suppliers.

Building a good relationship with them often leads to better pricing, faster material deliveries, and flexible credit terms when your cash flow gets tight. You should also treat local building inspectors with respect. Ask them questions and learn exactly what they look for during an inspection. Knowing what they want prevents expensive mistakes and keeps your project moving on schedule.

Ultimately, word of mouth is your best marketing tool. If you show up on time, keep the job site clean, and listen to the people around you, your local reputation will keep your pipeline full of high-quality referrals.

Step 7: Importance of professional cost estimation services

Accurately pricing your jobs is the most important skill you need to survive in the construction industry. If you underestimate your labor hours, you will either bid too high and lose the project or bid too low and pay out of pocket just to finish the job. Knowing exactly how to estimate construction costs helps you manage budgets effectively, significantly reduce your financial risks, and make much better daily business decisions.

Furthermore, when you hand a potential client a highly detailed, professional bid, it immediately builds client trust and teaches you exactly how to win construction bids consistently. However, doing manual takeoffs and building estimates takes dozens of hours every week. When you are trying to get a new business off the ground, you simply do not have that kind of time. This is exactly why smart business owners choose to outsource their cost estimation right from the start.

Partnering with a professional firm like ACON Engineering gives you a massive competitive advantage without the heavy overhead of hiring a full-time employee. Businesses that need estimating support on a project-by-project basis often benefit from professional Freelance Construction Estimating Services, allowing them to scale their estimating capacity without committing to permanent staff. ACON Engineering brings 15 years of industry experience to your business, providing certified estimators who handle all CSI trades.

Whether you need residential estimating, complex industrial estimating, or specialized MEP estimating, they deliver highly accurate numbers with a fast 24 to 48-hour turnaround. Their team covers the entire spectrum of pricing, offering everything from preliminary estimating and construction takeoffs to full bid management and estimating consulting. By outsourcing this process to ACON Engineering, you can save up to 60% compared to the cost of an in-house estimator.

This ensures your bids are always precise and profitable, allowing you to focus your energy on running your job sites and planning how to grow construction business revenue.

Step 8: Establish your web presence and launch your brand

Once your operations are set and you know how to price your jobs accurately, you have to get your name in front of local clients. Establishing a strong web presence is not just an extra marketing tactic; it is the digital face of your brand and often the very first impression a potential client gets of your company.

A professional, modern website immediately builds credibility and trust, showing prospects that you run a legitimate operation. Your site acts as a central hub where you can showcase photos of your completed projects, detail your specific capabilities, and capture new leads around the clock.

To actually reach more people and increase your visibility, you need to support your website with local SEO so your company ranks high when someone searches for a local contractor on Google. You should also set up active social media profiles where you can post valuable content, like daily progress photos from your job sites or quick advice on building maintenance.

Finally, you must actively manage your online reviews. Encouraging happy clients to leave positive ratings and responding professionally to all feedback proves that you stand behind your work.

How much does it actually cost to start a construction company?

Starting a construction business typically costs anywhere from $15,000 to $500,000. The exact amount depends heavily on the size of your operation and your specific trade. A specialty subcontractor who works out of a pickup truck and rents machinery might start on the lower end. A commercial general contractor buying heavy equipment, leasing office space, and hiring full crews will easily reach the half-million mark.

Because construction operates on long payment cycles, you also need a healthy cash buffer. You must have enough working capital in the bank to pay your crew and buy materials long before your first client pays their invoice. To figure out your exact budget, you have to break your expenses down into two main categories: initial startup costs and ongoing operating expenses.

One-time startup costs

These are the upfront expenses you have to pay before you can bid on your first project.

- Licenses and permits: You have to pay application fees for your state contractor board, local city registrations, and trade-specific certifications.

- Construction equipment: This covers buying your essential hand tools, safety gear, and securing down payments for any heavy machinery.

- Insurance setup: You must pay the initial premiums for general liability coverage, surety bonds, and workers’ compensation policies.

- Website design and branding: You need to pay for a clean, professional digital storefront and basic branding to capture early leads.

Ongoing operating costs

These are your regular, recurring bills that keep the company running month after month.

- Employee salaries and benefits: This includes the hourly wages for your field crew and the salaries for any administrative staff or estimators.

- Vehicles and transportation: You have to budget for monthly truck leases, fuel, vehicle insurance, and regular maintenance.

- Office rent and facilities: This covers the monthly lease for a physical office space or a secure storage yard for your materials and machinery.

- Marketing and advertising: You need a monthly budget for lead generation platforms, local ads, and maintaining your online presence.

- Tax preparation and accounting: You will pay ongoing fees to a CPA or bookkeeping service to manage your complex project-based payroll and quarterly taxes.

Final thoughts

Working on your own construction company takes serious effort, but it is one of the most practical ways to build real wealth. You are trading the safety of a standard paycheck for the freedom to run your own job sites, choose your own clients, and keep the profits.

Yes, the initial paperwork is hard, and managing your cash flow in those first few months will test your patience. But if you take it one step at a time, getting your licenses in order, setting up real job costing, and pricing your bids accurately, you will build a business that actually survives. Do not rush the foundation. Focus on getting your numbers right, treat your subcontractors well, and the revenue will naturally follow.

Frequently Asked Questions (FAQs)

Can you start a construction company with no experience?

It is possible, but it is highly risky. If you do not have field experience, you have to operate as a “paper contractor.” This means you strictly manage the business side and hire experienced subcontractors to do all the physical work. However, lacking hands-on experience makes it very hard to estimate job costs accurately or spot when a crew is cutting corners. Most successful owners spend at least a few years working in the trades before starting their own firm.

Can you start a construction company with no money?

You cannot start a construction business with literally zero dollars. Even if you start incredibly lean by renting tools and working out of your personal truck, you still have upfront costs. You have to pay for state licenses, business registration, and mandatory insurance policies. You can start small, but you cannot start for free.

How long does it take to start a construction company?

You can usually set up the legal and operational side of the business in 2 to 3 months. Registering your LLC, obtaining your tax IDs, and setting up a bank account take only a few days. The biggest delays almost always come from the state licensing board. Passing your contractor exams and waiting for your background checks and insurance paperwork to clear can easily take a month or two, depending on your local government.

What are some common challenges that arise when starting a construction business?

Cash flow is the number one challenge for new builders. Waiting 30 to 60 days for a client to pay an invoice while you still have to pay your crew every Friday can break a new company. Other common struggles include finding reliable subcontractors who show up on time, underpricing your bids due to bad math, and dealing with unexpected weather delays that disrupt your project timeline.

How do I land my very first construction project?

If you are trying to figure out how to get clients as a contractor, your first few jobs will almost always come from your existing personal and professional network. Before you spend money on internet ads, reach out directly to local real estate agents, property managers, and other busy contractors who might need to pass off some extra work. You can also start by taking on smaller repair jobs that the larger local companies ignore.

Tim C. is a construction estimating expert and Director at ACON Engineering, specializing in construction cost estimating, quantity takeoffs, and preconstruction planning. He has led thousands of successful project bids and helps contractors make informed, profitable decisions.